This week we look at how

Market Update | The Name’s Bond, Government Bond

Between the introduction of modern portfolio construction methods and until very recently, bonds played a key role in most investors’ multi-asset portfolios. In the past, you may have come across language referring to 70/30, 50/50, and 90/10 portfolios. Historically, this referred to a simple split between bonds and equities. For example, a growth portfolio would have 70% equities, 30% bonds. A balanced portfolio would have 50% equities and 50% bonds. As investment strategy has become more sophisticated, this definition has broadened to include other asset classes and a deeper understanding of what the numbers actually mean, particularly with respect to overall portfolio risk. Now, when a portfolio manager refers to a 70/30 portfolio, they will more than likely be referring to a general split between growth and defensive assets[1].

What Role do Bonds Play?

Bonds play a very important role in diversifying portfolio returns. At a high level, investing in a pool of diversified asset classes (rather than having all exposure in one basket) lowers portfolio volatility – helping smooth returns through time. Bonds have done a particularly good job of this role since the mid-1990s. The chart below shows the annual return to US 10-year bonds and the S&P500 since 1970[2]. Between 1970 and the mid-1990s, bond and equity market returns tended to move together. When equity prices rose, bond prices often followed suit. The inverse was also often true. Since 1996, we can see a structural shift in that relationship. In periods of substantial equity market weakness (the Tech Bubble, the Financial Crisis, Covid) bond prices (blue line) rose, helping offset the loss in equity markets. So far this year, bonds and equities have fallen together, an unusual combination.

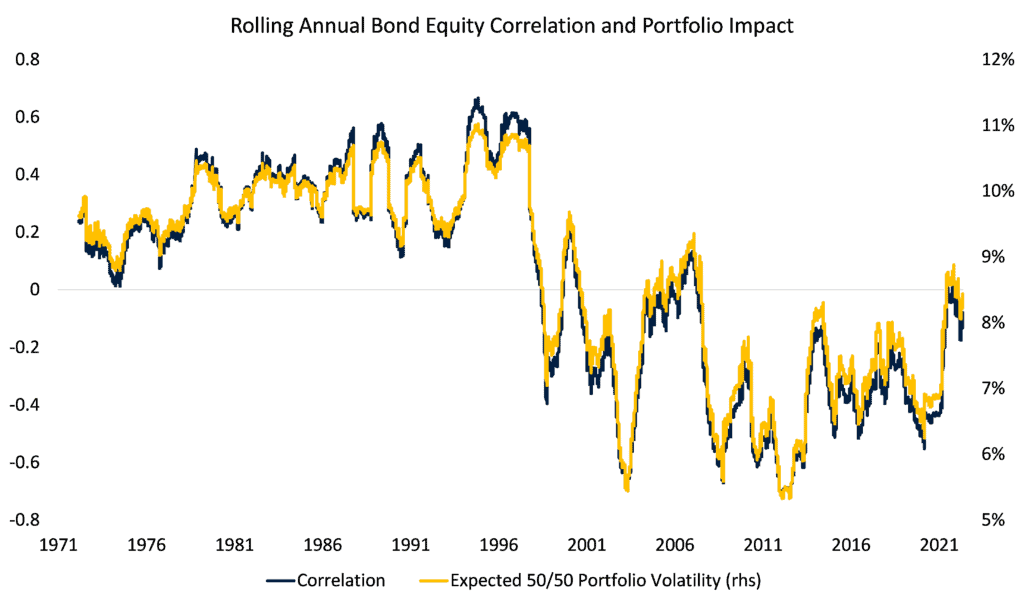

This can be shown in a more scientific way in the chart below, which plots the correlation between bond and equity returns. Correlation simply measures the degree to which things move together. Two cars driving next to each other atthe samespeedwould have a correlation of 1. The same car driving past a parked car would show zero correlation. Passing a car driving on the opposite side of the road at the same speed would show -1 correlation.

Pre-1996 bond and equity correlations were positive (prices moved together). Since then, they have been generally negative (one goes up, one goes down). We can demonstrate the particularly good job bonds have done at diversifying portfolios by showing the impact on expected portfolio volatility from the changing correlation through time. The yellow line below shows that the expected volatility of a balanced portfolio (50% equity, 50% bonds) fell from around 11% in 1995 to as low as 5.5% in 2012 entirely due to this fall in correlations. Put simply, balanced portfolios became less risky all on their own.

The obvious question from the above is: will correlations stay negative? In our view, that is largely dependent on whether inflation remains high or gets back under control. A large part of the reason why correlations were positive prior to 1996 was that inflation was highly variable and largely drove the economic cycle. Higher inflation necessitated higher interest rates, which lowered bond prices and also slowed the economy through higher borrowing costs (causing equity market weakness as earnings and valuations fell). When inflation was finally brought under control in the 1990s, movements in interest rates to combat inflation were much smaller in magnitude and financial excess became the dominant driver of market and economic corrections.

At the moment central banks appear extremely committed to re-containing inflation. In addition to this, a number of structural factors suggest inflation is unlikely to remain elevated in the decade ahead, particularly low potential economic growth and high global debt burdens. In line with this, we expect bond and equity correlations in the decade ahead to remain lower than they averaged in the 1970s and 1980s. As a result, bonds should continue to provide portfolio diversification and reduce overall portfolio volatility when times are tough for equity markets.

What Drives Bonds Returns?

For something which is very simple at face value (buy a bond, get some interest payments, get capital back at maturity), bonds can be extremely complicated. The global bond market is larger than the global equity market. The asset class includes instruments which vary from essentially risk free (short term US government bills) to extremely risky (recently defaulted Hong Kong listed property developer Sunac April 2023 bonds were trading at 19c on the dollar last week). Bonds can be asset backed, such as the mortgage-backed securities which were focal in the Financial Crisis. Interest payments can be fixed through the life of the bond or floating based on the prevailing central bank interest rate or even inflation linked. Bonds can be issued in a local or foreign currency. Some bonds can convert into equity. In the untimely event of a default, bond holders need to negotiate with other creditors and administrators to determine their share of asset recovery.

Like equities, the return to a bond portfolio can also be decomposed into a number of factors. For our purposes (given our portfolio is a diversified pool of many individual bonds) the key elements of a bond return are:

- The yield to maturity, effectively the coupon you get paid from holding a bond (yield)

- In a constant maturity portfolio (only holding 10-year bonds for example), the increase in price that normally occurs as a ten-year bond becomes a 9-year bond and is subsequently sold to buy a new 10-year bond (roll)

- The most important thing to remember about bonds is that when the interest rate goes up, the price goes down (duration)

- Any return to hedging foreign currency risk (hedging) which reflects the difference in prevailing interest rates between the two countries.

The chart below shows the impact of these four elements through time on a constant maturity portfolio of US 10-year government bonds for an Australian investor. There are a number of observations we can make based on this chart.

- The total return to the bond portfolio (green line) has become substantially less volatile over time.

- The volatility in the total return has been almost entirely driven by the impact of duration (yellow slice). Basically, volatile bond returns through time have been driven by movements in interest rates. As interest rates have become less volatile, so have bond returns.

- The return to bonds due to yield has fallen structurally since the 1980s. This makes sense as interest rates have fallen over this period. However, inflation has also fallen over this period, overstating the impact of this fall in real (inflation adjusted) terms.

- For an Australian investor, the impact of hedging returns has been very beneficial through time. This is because Australian interest rates have been generally higher than those in the US over the last 50 years. Buying an Australian bond rather than a US bond would see this return captured in higher yield.

- Roll has provided a small, but generally positive boost to returns through time.

Going forward, we expect the return to government bonds to remain relatively low. The grey bars in the chart below show the decomposition expected US bond returns in our most likely capital market return scenario (this, along with others, will be featured as part of our 2022 Strategic Asset Allocation Review). Overall, returns are expected to be a little lower than the post Financial Crisis period, largely driven by a loss in return to hedging. The Australian cash rate is not expected to be structurally higher than the US Federal Funds Rate over the next decade. Still, in an environment where global equities are expected toreturn ~7%, an expected ~3% return to a defensive asset with a negative correlation to equities has a place in a diversified portfolio.

Tactically Allocating to Bonds

After a long period of being underweight, we recently moved overweight bonds in early April this year. The increase in interest rates since August 2020 has seen longer dated bonds suffer their worse cumulative drawdown since 1980 (yellow line in chart below).

We think on balance interest rates will not rise much more from this point, suggesting the drawdown is near its worst. There are a number of reasons for this.

- A significant number of rate hikes are currently priced into the market for the US (along with most other major advanced economies). Unless we have renewed global supply chain disruptions, this should be sufficient to combat inflation.

- Economic growth will slow over the next year due to declining fiscal stimulus, Covid lockdowns in China, declining real household incomes and the increase in interest rates which has already occurred.

- We expect inflation to ease reflecting a peak in the inventory cycle across the US (businesses have restocked after supply chain problems), and as base effects related to the normalisation of pandemic related price increases fall out of the annual inflation calculation.

Slower growth and moderating inflation are a positive combination for bonds. In addition, the increase in yields which occurred since August 2020 has provided a large buffer from which bonds can rally should equity markets continue to correct – improving their diversifying potential.

[1] The split could also reference the net amount of “equity like” or “equity equivalent” exposure in a portfolio or

[2] This is the return to a constant maturity bond position, which will be a little different to a held to maturity portfolio. Between 1970 and 1980, bond index returns calculated based on prevailing interest rates and assuming bond duration of 6.2 years. Prior to 1975 the Australian cash rate is proxied by 3M bank accepted bills. S&P500 returns prior to 1988 do not include dividends.

Disclaimer

Prepared by Drummond Capital Partners (Drummond) ABN 15 622 660 182, a Corporate Authorised Representative of BK Consulting (Aust) Pty Ltd (AFSL 334906). It is exclusively for use for Drummond clients and should not be relied on for any other person. Any advice or information contained in this report is limited to General Advice for Wholesale clients only.

The information, opinions, estimates and forecasts contained are current at the time of this document and are subject to change without prior notification. This information is not considered a recommendation to purchase, sell or hold any financial product. The information in this document does not take account of your objectives, financial situation or needs. Before acting on this information recipients should consider whether it is appropriate to their situation. We recommend obtaining personal financial, legal and taxation advice before making any financial investment decision. To the extent permitted by law, Drummond does not accept responsibility for errors or misstatements of any nature, irrespective of how these may arise, nor will it be liable for any loss or damage suffered as a result of any reliance on the information included in this document. Past performance is not a reliable indicator of future performance.

This report is based on information obtained from sources believed to be reliable, we do not make any representation or warranty that it is accurate, complete or up to date. Any opinions contained herein are reasonably held at the time of completion and are subject to change without notice.